7 High-Yield Dividend Stocks for Steady Income in 2026

If you’re looking for reliable income in 2026, high-yield dividend stocks can be a smart choice. With S&P 500 yields at just 1.1% and 10-year Treasury rates at 4.2%, these stocks offer a way to earn more while maintaining stability. Here’s a quick rundown of seven solid options:

- Fortis (FTS.TO): 3.6% yield, 52 years of dividend growth, and a focus on regulated utility assets.

- Toromont Industries (TIH.TO): Low 1.17% yield but a 35-year dividend growth streak and a conservative payout ratio.

- Canadian National Railway (CNR.TO): 2.6% yield with 30 years of increases and strong operational efficiency.

- Canadian Natural Resources (CNQ.TO): 4.97% yield, 25 years of growth, and a disciplined capital return strategy.

- Emera (EMA.TO): 6.0% yield, 19 years of growth, and a focus on regulated utilities.

- National Bank (NA.TO): 3.3% yield, 16 years of growth, and a diversified revenue base.

- Alimentation Couche-Tard (ATD.B.TO): 1.16% yield with a strong history of dividend growth (25% over 5 years).

Each stock offers a mix of yield, growth, and reliability, catering to different financial goals. Whether you’re prioritizing immediate income or long-term dividend growth, these companies provide options across various sectors like utilities, energy, and finance.

Key Takeaway: Choose stocks based on your priorities – higher yields for retirees or growth-focused picks for younger investors. Always check payout ratios and financial health to avoid unstable dividends.

The Top 5 High Yield Dividend Stocks for 2026!

sbb-itb-484be5d

1. Fortis (FTS.TO)

Fortis stands out as a reliable utility stock in North America, offering a dividend yield between 3.6% and 3.7% as of early 2026, which surpasses the average yield of the S&P 500.

This company has an impressive history of consistency, with 52 consecutive years of dividend increases. Nearly all (99%) of its earnings are derived from regulated utility assets, providing stable and predictable cash flows that are largely shielded from economic fluctuations.

Fortis has a clear growth plan in place. Management is aiming for 4–6% annual dividend growth through 2030, powered by a $28.8 billion capital investment plan spanning 2026 to 2030. This plan is expected to drive a 7% compound annual growth rate (CAGR) in its rate base while maintaining a stable adjusted payout ratio of 72.7%.

The company is also well-positioned to capitalize on the rising demand for electricity, fueled by the growth of data centers and industrial electrification. One example of this is its Tucson Electric Power subsidiary, which has secured a long-term contract starting in 2027 to supply up to 300 megawatts of power, with the potential to expand by an additional 500–700 megawatts.

With its strong fundamentals, Fortis offers a compelling option for investors seeking steady dividends and predictable growth in a world that’s increasingly reliant on electricity.

2. Toromont Industries (TIH.TO)

Toromont Industries currently offers a dividend yield of 1.17%. While this may not appeal to those seeking high-yield investments, the company’s 35-year streak of dividend growth is where it truly shines. This impressive track record highlights its ability to consistently reward shareholders, regardless of economic ups and downs.

What makes these dividends even more appealing is their sustainability. Toromont maintains a conservative payout ratio of 30.06%, meaning it distributes less than one-third of its earnings as dividends. This leaves plenty of room for future increases, even during challenging times. For those who invested early, the yield on cost has grown to an impressive 9%, showcasing the strength of its business model over time.

Toromont’s stability is further reinforced by its well-diversified operations. The company operates in two main segments: the Equipment Group, which serves industries like mining, construction, and infrastructure, and CIMCO, which focuses on industrial refrigeration. A key advantage is that 97% of its revenue is generated within Canada, reducing exposure to cross-border risks. Additionally, the Equipment Group benefits from higher-margin parts and service work, which helps maintain steady performance even during economic downturns.

Financially, Toromont remains strong. In Q3 2025, the company reported revenue of $1.315 billion and operating income of $189.5 million, supported by a robust backlog of $1.3 billion. This backlog provides a solid foundation for continued growth in dividends. In fact, the company recently announced an 8.3% dividend increase, reinforcing its commitment to delivering long-term value to shareholders.

3. Canadian National Railway (CNR.TO)

Canadian National Railway (CN) currently offers a dividend yield of 2.6%–2.7%, which is notably higher than its 10-year average of 1.8%. This yield, coupled with an impressive streak of 30 consecutive years of dividend increases, highlights CN as a solid choice for income-focused investors. For those looking for a reliable entry point, this combination of yield and consistency is hard to overlook.

CN’s operational strengths add further confidence to its long-term prospects. Its extensive 20,000-mile tri-coastal network connects the Atlantic, Pacific, and Gulf coasts, creating significant barriers for competitors. Historically, CN has been able to achieve pricing gains of 3%–4% above the inflation rate, showcasing its ability to maintain profitability in varying economic conditions.

In addition to its operational resilience, CN remains committed to rewarding its shareholders. The company maintains a sustainable dividend policy, supported by a moderate payout ratio of around 35%. In Q3 2025, CN reported revenue of C$4.17 billion and an operating income of C$1.61 billion, reflecting a 6% year-over-year growth. Its operating ratio stood at an efficient 61.4%. While recent dividend growth has slowed to 5%, compared to its 10-year average of 13%, this appears to be a short-term issue. The decline of about 8%–9% in 2025, attributed to uncertainty surrounding Canada-U.S. trade negotiations, has impacted growth temporarily [16,23]. Analysts project that as trade agreements become clearer in 2026, dividend growth could recover, potentially reaching 10% by 2027.

CN also raised its quarterly dividend to C$0.89 per share and repurchased approximately 8 million shares for C$1 billion during Q3 2025. With institutional investors holding about 80% of the company’s outstanding shares and the stock trading at a price-to-earnings ratio of 18x – below its historical average of 21x – CN presents a blend of income stability and long-term growth potential for patient investors.

4. Canadian Natural Resources (CNQ.TO)

Canadian Natural Resources (CNQ) offers a forward dividend yield of 4.97%, backed by an impressive 25-year streak of dividend increases and an annualized dividend growth rate of 21%. This level of consistency stands out, especially in the often-volatile energy sector, where maintaining payouts during downturns can be a significant challenge.

A key strength of CNQ is its low-cost, long-life asset base, which supports a reserve life index of around 32 years. In Q3 2025, the company demonstrated efficient operations, reporting natural gas production costs of C$1.16 per Mcf and oil sands mining expenses of C$21.29 per barrel. This low breakeven cost enables CNQ to generate solid free cash flow even when oil prices are in the US$50–$59 per barrel range.

The company follows a "disciplined growth plus aggressive capital returns" strategy. CNQ adjusts its shareholder return policy based on its net debt levels: when net debt hits $15 billion, 60% of free cash flow is returned to shareholders, and if it drops to $12 billion, that allocation increases to 75%. This approach has allowed CNQ to return C$6.2 billion to shareholders as of November 5, 2025, with C$4.9 billion distributed through dividends.

Looking ahead to 2026, CNQ plans to invest $6.42 billion in capital expenditures targeting a 3.2% production increase. The company has also announced a quarterly dividend of C$0.5875 per share, payable on January 6, 2026. With a liquidity position of approximately $4.8 billion and the ability to remain profitable even if WTI prices average around $50 per barrel, CNQ offers a reliable income option for investors navigating the unpredictable energy market.

5. Emera (EMA.TO)

Emera offers an impressive 6.0% dividend yield as of January 18, 2026 – more than double the electric utilities industry median of 2.8%. This regulated utility operates across Canada, the U.S., and the Caribbean, delivering steady revenue regardless of economic fluctuations. With a 19-year streak of consecutive dividend increases, Emera has demonstrated consistent reliability, although recent growth has been intentionally modest.

The company’s dividend is well-supported by earnings, with a payout ratio of 78.4%. Management has chosen a cautious path, prioritizing financial stability over aggressive growth. They’ve set their sights on annual dividend increases of just 1–2% while executing an ambitious $8.8 billion capital program. To strengthen its financial footing, Emera has made strategic moves, such as selling the Labrador Island Link, which reduced holding company debt by $957 million.

Emera’s regulated business model ensures the stability income-focused investors value. In the first three quarters of 2025, operating cash flow climbed 23%, and adjusted earnings rose 9% year-over-year to $0.88 per share. Looking ahead, the company plans to invest $20 billion from 2026 through 2030, with nearly 80% allocated to its Florida operations. This investment aims to drive a 7–8% rate base growth through 2030. These strong financial and operational metrics reflect a balanced approach to both yield and growth.

For investors seeking steady income, Emera’s 6.0% yield, combined with modest 1–2% annual dividend increases, offers an attractive option. Additionally, recent interest rate cuts are expected to lower borrowing costs, further enhancing cash flow available for distributions.

Adding to its stability, Emera plans to sell New Mexico Gas Company for $1.25 billion, a move that will further solidify its position as a top choice for income-focused investors. While its five-year compound dividend growth rate is 1.8%, the current yield surpasses the five-year average of 4.9%, making Emera a compelling high-yield option for those prioritizing immediate income over rapid dividend growth.

6. National Bank (NA.TO)

National Bank brings a fresh layer of diversity to this high-yield lineup, blending financial discipline with a growing presence across Canada. As of January 18, 2026, the bank offers a dividend yield of 3.3%, supported by an annual dividend of C$4.40 per share. With a conservative payout ratio of 42.84% and a five-year earnings per share CAGR of 8%, it presents a solid option for income-focused investors.

In December 2025, National Bank raised its quarterly dividend from C$1.18 to C$1.24 per share, marking a 5.1% increase. Over the past five years, its dividend has grown at an impressive 11% compounded annual growth rate. This consistent growth is backed by strong earnings, including a 41% rise in Capital Markets revenue and an 18% increase in Wealth Management revenue in Q4 2025.

The bank’s fiscal 2025 results highlight its financial resilience. It ended the year with a Common Equity Tier 1 (CET1) ratio of 13.8%, comfortably exceeding regulatory requirements. Adjusted net income for Q4 2025 climbed 25% year-over-year to C$1.16 billion, while revenue surged by 24–26% to C$3.7 billion. A payout ratio of 45.6% for fiscal 2025 signals the potential for further dividend increases. These results position National Bank for continued growth and strategic moves to diversify its revenue streams.

Recent expansions have reshaped National Bank from a Quebec-centric institution into a stronger national player. Its 2025 acquisition of Canadian Western Bank and Laurentian Bank‘s retail portfolios have significantly broadened its geographic reach, reducing Quebec’s contribution to 2025 revenue to 45%. CEO Laurent Ferreira commented:

the bank met all its medium-term financial objectives in 2025 while closing its largest-ever acquisition, CWB, and entering 2026 with a broader national footprint and more diversified earnings mix.

For investors seeking reliable income, National Bank’s consistent dividend growth, strong financial performance, and attractive trailing P/E ratio of 12.89 make it a compelling choice.

7. Alimentation Couche-Tard (ATD.B.TO)

Alimentation Couche-Tard focuses on growing dividends and repurchasing shares rather than offering a high current yield. At present, its dividend yield stands at 1.16%. In November 2025, the company raised its quarterly dividend by 10.3% to C$0.215 per share, marking an impressive 14-year streak of annual increases.

Over the past decade, Couche-Tard has consistently delivered dividend growth rates of 25%–26% across 3-year, 5-year, and 10-year periods. This remarkable growth is supported by the company’s stable earnings. In fact, diluted earnings per share (EPS) have only dipped twice in the last 15 years – by 1% and 6%, respectively. A low payout ratio further strengthens its ability to sustain and grow dividends in the future.

In late 2025, Couche-Tard returned capital to shareholders by repurchasing C$1.19 billion worth of shares, equating to 22,700,000 shares or 2.39% of its float. Around the same time, the company reported quarterly net income of US$740.6 million and earnings per share of US$0.79. Looking ahead, revenue is projected to reach US$77.0 billion with earnings of US$3.1 billion by 2028.

To navigate market challenges, Couche-Tard is leaning into higher-margin offerings such as food services and private-label products. Additionally, it has embraced the energy transition, achieving a 9% market share in the EV charging markets of Norway and Sweden, 13% in Denmark, and expanding further into Germany and the Benelux region. Simply Wall St highlights:

Couche-Tard’s resilient business model, strong earnings, cash flows, and low payout ratio further support the idea that its dividend-growth streak could continue for years to come.

For investors seeking a balance between income growth and capital appreciation, Couche-Tard offers an attractive opportunity. Analysts estimate its fair value at approximately CA$85.30, compared to recent trading levels near CA$73.80. This suggests room for both income growth and value appreciation. Its forward-thinking strategy cements its position as a standout choice in an income-focused portfolio.

Stock Comparison Table

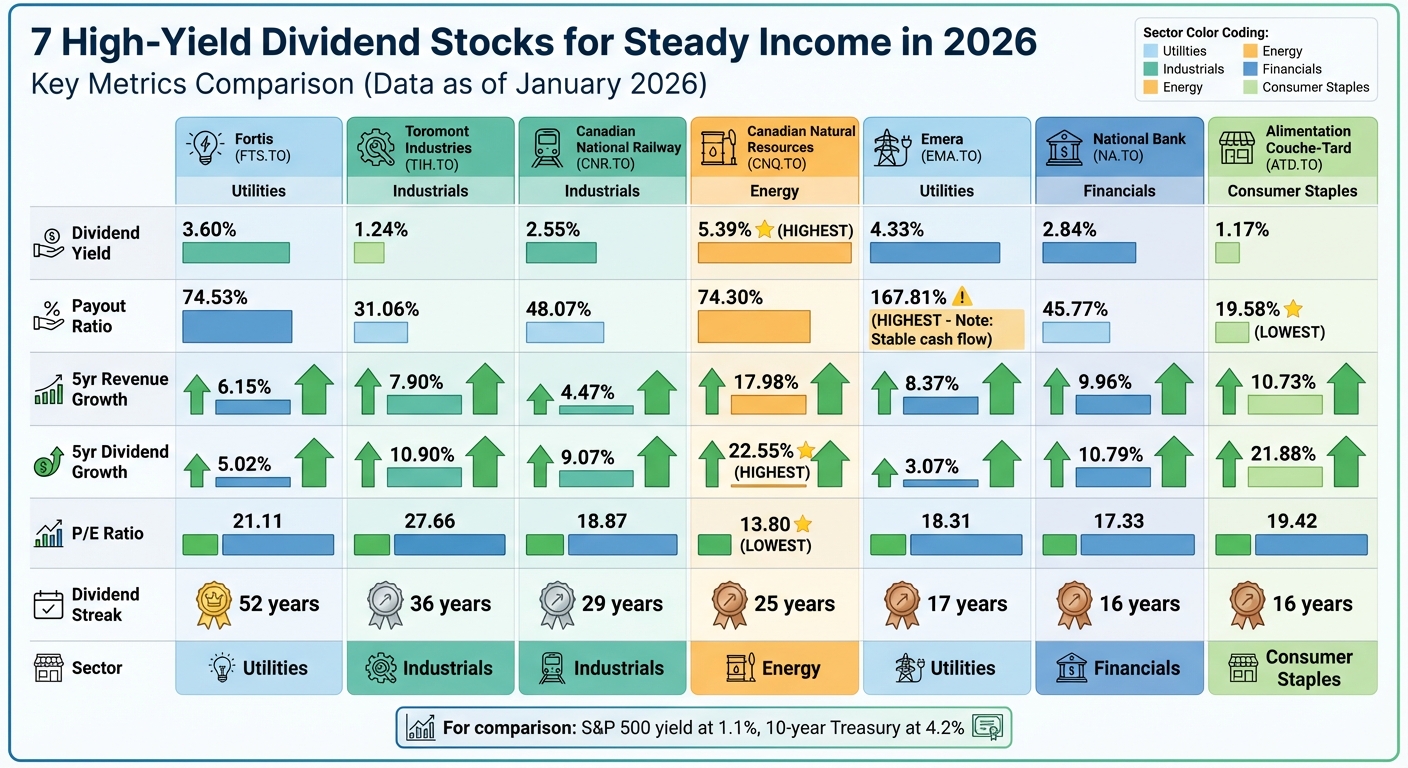

7 High-Yield Canadian Dividend Stocks Comparison 2026

Below is a table summarizing key metrics for these dividend stocks. Each stock offers a different mix of yield, growth potential, and dividend consistency.

| Stock (Ticker) | Div. Yield | Payout Ratio | 5yr Rev. Growth | 5yr Div. Growth | P/E Ratio | Div. Streak (Years) |

|---|---|---|---|---|---|---|

| Fortis (FTS.TO) | 3.60% | 74.53% | 6.15% | 5.02% | 21.11 | 52 |

| Toromont (TIH.TO) | 1.24% | 31.06% | 7.90% | 10.90% | 27.66 | 36 |

| CN Railway (CNR.TO) | 2.55% | 48.07% | 4.47% | 9.07% | 18.87 | 29 |

| CN Resources (CNQ.TO) | 5.39% | 74.30% | 17.98% | 22.55% | 13.80 | 25 |

| Emera (EMA.TO) | 4.33% | 167.81% | 8.37% | 3.07% | 18.31 | 17 |

| National Bank (NA.TO) | 2.84% | 45.77% | 9.96% | 10.79% | 17.33 | 16 |

| Couche-Tard (ATD.TO) | 1.17% | 19.58% | 10.73% | 21.88% | 19.42 | 16 |

(Data as of January 2026) [33]

Here’s a closer look at some standout metrics from the table:

- Canadian Natural Resources (CNQ.TO) leads the pack with the highest dividend yield at 5.39%, combined with impressive five-year dividend growth of 22.55%. It’s a strong choice for those seeking both income and growth.

- Couche-Tard (ATD.TO) offers a modest 1.17% yield but shines with a very low payout ratio of 19.58% and a five-year dividend growth rate of 21.88%. This indicates room for future dividend increases.

- Fortis (FTS.TO) stands out with an incredible 52-year streak of dividend increases, underlining its reliability as a dividend payer.

- Emera (EMA.TO), while offering a solid 4.33% yield, has a concerning payout ratio of 167.81%, meaning its dividends currently exceed its accounting earnings. However, its regulated utility operations provide stable cash flow, which may help sustain payouts.

- Toromont (TIH.TO) and National Bank (NA.TO) strike a balance with moderate yields (1.24% and 2.84%, respectively), steady dividend growth, and conservative payout ratios under 50%, making them appealing for long-term stability.

Each stock brings its own strengths, catering to different investment goals, whether it’s high yield, growth potential, or dividend reliability.

Conclusion

Spreading your investments across different sectors can help protect your portfolio from downturns in specific industries. The stocks mentioned here cover a range of sectors, including Utilities, Industrials, Energy, Financials, and Consumer Staples.

It’s important to strike a balance between high dividend yields and the potential for growth. For instance, while Canadian Natural Resources offers a strong yield, Couche-Tard has shown notable dividend growth over the past five years. This kind of growth can lead to a significant boost in income over time, highlighting the importance of sustainable payouts.

Take a close look at each company’s payout ratio and overall financial health to ensure dividends can be maintained. A payout ratio under 50% often indicates room for future increases, whereas ratios above 100% might warrant a deeper dive into cash flow stability.

Tailor your stock picks to align with your financial goals. Retirees might prioritize higher-yielding stocks like Canadian Natural Resources or Emera, while younger investors could focus on stocks with strong dividend growth potential, such as Couche-Tard or National Bank. These strategies reflect the insights of top market analysts.

"The best investors are those who focus on fundamentals, remain steady through volatility, and filter out market noise." – Daniel Foelber, Contributing Analyst, The Motley Fool

With the S&P 500 offering record-low yields of around 1.1% in early 2026, these stocks stand out as compelling options for income-focused investors seeking diversification.

FAQs

What should I consider when deciding between high-yield and dividend-growth stocks?

When deciding between high-yield stocks and dividend-growth stocks, it’s important to start by examining the dividend yield and payout ratio. High-yield stocks can deliver a strong income stream right away, but a high payout ratio might signal that the company is stretching its finances. This could lead to dividend cuts if earnings take a hit. To minimize risk, focus on companies with solid financial health and sustainable payout ratios.

On the other hand, dividend-growth stocks emphasize gradual, consistent increases in their payouts. These companies typically show steady earnings growth, robust cash flow, and a history of regularly raising dividends. They’re a great option for investors looking for long-term growth while still earning a moderate income.

The best choice depends on your investment goals and how much risk you’re comfortable with. High-yield stocks work well for those needing immediate income but may come with more ups and downs. Dividend-growth stocks are better suited for those aiming to combine steady income with long-term capital growth.

What should I look at to determine if a dividend stock is financially stable?

To assess the financial health of a dividend stock, pay attention to several critical aspects:

- Dividend yield and payout ratio: A high yield might catch your eye, but it’s crucial to examine the payout ratio – this represents the percentage of earnings distributed as dividends. A payout ratio under 100% usually suggests the company has room to maintain or even increase its dividends.

- Free cash flow: Companies with steady, positive free cash flow are in a stronger position to fund their dividends without leaning on debt or outside financing.

- Debt and leverage: Keep an eye on the debt-to-equity ratio and interest coverage. A manageable level of debt and the ability to comfortably cover interest payments indicate the company is better equipped to handle economic downturns without jeopardizing its dividend.

It’s also wise to seek out companies with consistent or growing earnings over time, as this underpins long-term dividend reliability. Firms with high return on equity (ROE) and solid profit margins tend to operate more efficiently, which supports their ability to sustain dividend payouts. By weighing these factors, you can pinpoint dividend stocks that are more likely to deliver dependable income for the long haul.

Why should dividend investors diversify their portfolio across different sectors?

Diversifying your dividend stock investments across various sectors can help you manage risk while maintaining a steady income stream. Economic conditions impact industries differently – some sectors might flourish while others struggle. By spreading your investments, you can offset losses in one area with gains in another.

On top of that, some sectors tend to deliver higher dividend yields, while others focus more on growth. A balanced portfolio lets you tap into both opportunities, offering a more dependable and resilient income over time.