How to Build a Dividend Portfolio for Passive Income

Building a dividend portfolio is one of the most effective ways to generate passive income. Here’s the quick rundown:

- Choose Quality Dividend Stocks: Focus on companies with sustainable payouts. Look for a dividend yield between 2%-5%, a payout ratio below 60%, and consistent dividend growth over 10+ years.

- Diversify Across Sectors: Spread investments across 5-7 industries to reduce risk. Include a mix of high-yield stocks, Dividend Aristocrats, and dividend growth stocks.

- Evaluate Financial Health: Check key metrics like debt-to-equity ratio (<2.0), current ratio (>2.0), and free cash flow to ensure dividend sustainability.

- Reinvest Dividends: Use Dividend Reinvestment Plans (DRIPs) to compound growth over time.

- Monitor and Adjust: Review your portfolio every 6-12 months to rebalance and ensure it aligns with your income goals.

A well-built portfolio, diversified across 20-30 stocks, can provide reliable income and long-term growth. For example, a $300,000 portfolio with a 4% yield could generate $1,000 monthly. Stay consistent, reinvest dividends, and avoid chasing unsustainable high yields.

The Simple Dividend Portfolio I’d Start With in 2026

Step 1: Choose Quality Dividend Stocks

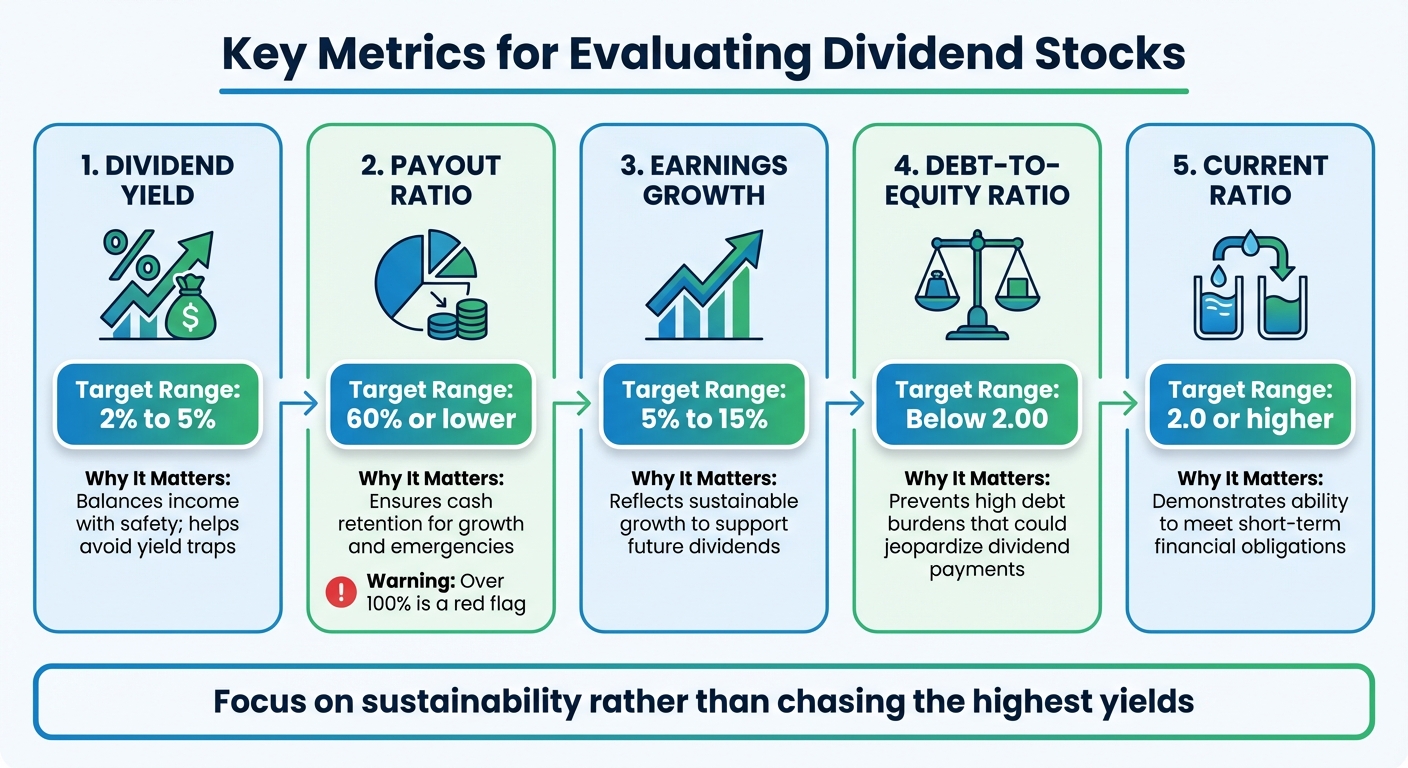

Key Metrics for Evaluating Dividend Stocks

Key Metrics to Evaluate Dividend Stocks

When selecting dividend stocks, it’s essential to focus on financial metrics that confirm both the sustainability and growth potential of dividends. Dividend yield is a good place to start. This is calculated by dividing the annual dividend by the current stock price. While a higher yield might seem appealing, be cautious – if a stock’s yield is far above its peers or exceeds the current yield on the 10-year Treasury note, it could be a "yield trap." Often, this happens when a company’s stock price has dropped significantly, signaling potential financial trouble rather than strong profitability.

Another critical metric is the payout ratio, which shows the percentage of net income or free cash flow allocated to dividends. A payout ratio of 60% or less is generally considered safe, as it leaves room for the company to weather economic challenges. If the ratio exceeds 100%, it’s a red flag that the dividend may not be sustainable.

The dividend growth rate is just as important as the current yield. Companies that have consistently increased their dividends over 10, 25, or even 50 years demonstrate financial strength and a commitment to rewarding shareholders. Look for businesses with long-term earnings growth projections between 5% and 15%. Growth rates beyond 15% can be unstable, potentially leading to disappointments that negatively affect stock prices.

Other financial metrics also play a role in assessing a company’s stability. For instance, the debt-to-equity ratio should ideally be below 2.00, as excessive debt can force a company to prioritize debt payments over dividends during tough times. A current ratio of 2.0 or higher indicates that the company can comfortably meet its short-term financial obligations. Lastly, check that the company’s free cash flow – cash remaining after capital expenditures – can adequately support its dividend program. Without sufficient free cash flow, dividends may be at risk.

| Metric | Target Range | Why It Matters |

|---|---|---|

| Dividend Yield | 2% to 5% | Balances income with safety; helps avoid yield traps |

| Payout Ratio | 60% or lower | Ensures cash retention for growth and emergencies |

| Earnings Growth | 5% to 15% | Reflects sustainable growth to support future dividends |

| Debt-to-Equity | Below 2.00 | Prevents high debt burdens that could jeopardize dividend payments |

| Current Ratio | 2.0 or higher | Demonstrates the ability to meet short-term financial obligations |

With these metrics in mind, you can use screening tools to identify potential dividend stock candidates efficiently.

Stock Screening Tools and Techniques

These metrics are the foundation for filtering stocks using screening tools that align with your dividend investment strategy. Stock screeners are invaluable for narrowing down the thousands of available companies to those that meet your income goals and risk preferences. Many major brokerage platforms, such as Charles Schwab and Fidelity, offer free built-in screeners that allow you to sort stocks by criteria like payout ratio, current ratio, sector, and dividend yield.

For more specialized dividend research, platforms like Dividend.com provide dedicated tools. These include screeners for common stocks, ADRs, REITs, and MLPs, along with proprietary ratings for dividend reliability and yield potential. Dividend.com rates stocks on a 1–5 scale across categories like dividend quality, earnings growth, and price momentum. While the basic screener is free, a premium membership offers access to advanced ratings and dividend estimates.

To simplify your search, consider starting with pre-screened lists such as the Dividend Aristocrats (S&P 500 companies with 25+ consecutive years of dividend increases) or Dividend Achievers (companies with at least 10 years of consistent increases). As of early 2025, the median dividend yield for Dividend Aristocrats was approximately 2.25%. These companies have proven their ability to maintain and grow dividends through various economic conditions. Additional resources like the Value Line Investment Survey and Mergent’s Dividend Achievers can also help you identify stocks with strong dividend histories.

When using screeners, focus on sustainability rather than chasing the highest yields. For instance, set filters for a payout ratio of 60% or less and a current ratio of 2.0 or higher. Diversifying across five to seven industries – such as utilities, healthcare, and consumer staples – can also help reduce sector-specific risks.

Step 2: Evaluate Dividend Sustainability and Growth

Review Dividend Payment History

A company’s dividend history can reveal a lot about its priorities. A track record of at least 10 years of consistent or growing payouts is a strong indicator that management is committed to rewarding shareholders – even during tough economic times. This resilience becomes especially evident during recessions or market downturns, when some companies manage to maintain or even increase their dividend payments.

To start your research, consider well-known benchmarks like the Dividend Aristocrats and Dividend Achievers. For example, between 2011 and 2021, Bank of America (BAC) dramatically increased its quarterly dividend from $0.01 per share to $0.21 per share. This 20-fold jump boosted its yield from 0.1% to 2.2% over the decade.

"Companies that raise their dividends steadily over time tend to continue doing so in the future, assuming the business continues to be healthy." – Investopedia

Once you’ve identified companies with a solid dividend history, the next step is to evaluate whether those dividends are sustainable by digging into their financial health.

Analyze Payout Ratios and Financial Strength

A strong dividend history is only part of the equation. To ensure that these payouts are sustainable, you need to examine key financial metrics. Start with the payout ratio, which measures the percentage of earnings paid out as dividends. Ideally, this ratio should stay at or below 60%, leaving room for the company to navigate financial difficulties. If the payout ratio exceeds 75%, it’s a red flag, and anything over 100% means the company is paying out more than it earns – a potential sign of trouble ahead.

However, relying solely on earnings isn’t enough. Free cash flow (FCF) is a more reliable measure of a company’s ability to sustain dividends. For example, Apple (AAPL) paid $1.04 per share in dividends while earning $6.43 per share, resulting in a conservative payout ratio of just 16.17%. This leaves plenty of room for future growth.

"Don’t let a company fool you with accounting profits (Net Income). A dividend is only safe if it’s covered by Free Cash Flow (FCF)." – Investing.com

Beyond cash flow, consider the company’s overall financial strength. Look for a debt-to-equity ratio below 2.00 and credit ratings of "A" or higher, as these indicators suggest lower dividend risk and solid financial footing. A great example is Realty Income (O), which, as of late 2025, maintained a 5.3% yield and had increased its dividend for 30 consecutive years, showcasing both stability and growth.

Step 3: Diversify Your Dividend Portfolio

Spread Investments Across Sectors

Relying heavily on one or two industries is a gamble. If a single sector takes a hit, your income could be in jeopardy. To reduce this risk, spread your investments across at least five to seven industries. For instance, if energy stocks slash dividends due to falling oil prices, sectors like healthcare, utilities, or consumer staples can help maintain your income stream.

As of January 2025, the risks of concentrating too much in a few sectors have become increasingly evident, especially with passive index funds. By building your own portfolio and deliberately spreading investments across stable sectors (like utilities and healthcare) and cyclical ones (such as financial services and energy), you can better shield your income during economic downturns.

A well-rounded portfolio typically includes 20–30 stocks. This helps ensure that even if a few companies cut or eliminate their payouts, your overall income stays steady. To manage risk, keep any single stock to less than 5% of your total portfolio.

Add International Dividend Stocks

Once your portfolio is diversified across sectors, consider branching out into international markets. Depending only on U.S. companies limits your options and increases vulnerability to domestic economic slowdowns. International dividend stocks bring exposure to different economies, currencies, and industries that often move independently of the U.S. market. For example, while the S&P 500’s average yield was around 1.3% in 2024, many international dividend ETFs offered yields over 4%.

Take the Vanguard International High Dividend Yield ETF (VYMI), which delivers a 3.58% annual yield across 1,508 stocks with a low 0.17% expense ratio. If you’re looking for higher income, the iShares International Select Dividend ETF (IDV) offers a 4.83% yield, though it’s more concentrated with 101 holdings and comes with a 0.50% expense ratio. These ETFs provide instant global diversification without requiring you to research individual foreign companies.

However, remember that foreign dividends may face withholding taxes of up to 30%. To maximize your earnings, consider holding international dividend stocks in tax-advantaged accounts like IRAs. To manage risk, it’s wise to keep your international exposure below 25% of your total portfolio.

Allocation Strategies for Different Stock Types

Diversifying across domestic and international markets strengthens your portfolio, but balancing different types of dividend payers is just as important. A strong portfolio includes three key categories: high-yield stocks for immediate income, Dividend Aristocrats for reliability, and dividend growth stocks to combat inflation.

- High-yield stocks: These typically offer yields between 4% and 6%, providing strong current income. However, they come with a higher risk of dividend cuts.

- Dividend Aristocrats: Companies with 25+ years of consecutive dividend increases. They offer stability with a median yield of around 2.25%.

- Dividend growth stocks: These often start with lower yields but increase payouts over time, helping protect your purchasing power in the long run.

By blending these strategies, you can balance immediate income needs with future growth potential.

| Strategy Type | No. of Stocks | Risk Level | Management Required |

|---|---|---|---|

| High-Yield Focus | 5 to 10 stocks | Higher (risk of cuts) | High (frequent monitoring) |

| Broad Diversification | 20 to 30 stocks | Lower (spread across sectors) | Moderate (quarterly reviews) |

| ETF Approach | Single Fund | Moderate (market-dependent) | Low (fund handles management) |

Your allocation should align with your income goals and risk tolerance. For example, if you’re aiming for $1,000 in monthly income at a 4% yield, you’d need approximately $300,000 invested. Younger investors may want to prioritize dividend growth stocks, while retirees often favor a mix that leans toward stable, high-yield options. And don’t forget to steer clear of yield traps, as discussed earlier.

sbb-itb-484be5d

Step 4: Reinvest Dividends and Track Performance

How to Reinvest Dividends

Building a diversified dividend portfolio is just the beginning. To maximize your returns, reinvesting dividends is key. With Dividend Reinvestment Plans (DRIPs), your cash dividends are automatically used to purchase more shares, creating a compounding effect that can significantly boost growth. The best part? Major brokers like Fidelity and Schwab typically offer DRIPs at no extra cost. Unlike standard trades, DRIPs also let you buy fractional shares, ensuring every penny is reinvested immediately.

Here’s why reinvesting matters: Over a 20-year period, reinvesting dividends can increase your total returns by about 47% compared to simply taking the cash. That’s a huge difference, especially when compounded over decades.

However, keep in mind that reinvested dividends are taxable in the year they’re received unless you’re investing through a tax-advantaged account like a Roth IRA. To avoid this "tax drag", consider holding dividend-paying stocks in retirement accounts where they can grow tax-free. If you earn at least $10 in dividends during the calendar year, your broker will send you a Form 1099-DIV for tax reporting.

Once you’ve set up DRIPs, the next step is to monitor your portfolio regularly to ensure everything stays on track.

Monitor and Adjust Your Portfolio

Keeping an eye on your portfolio is essential for maintaining balance and performance. A good rule of thumb is to review your portfolio every 6–12 months. This approach helps you avoid overreacting to short-term market swings while ensuring your investments remain aligned with your goals.

During your review, check that your holdings are not only paying dividends but also growing them consistently. Companies with payout ratios between 30% and 60% typically have enough flexibility to maintain their payments even during challenging periods.

Another important aspect to watch is your portfolio’s allocation. If a single stock grows to represent more than 5% of your portfolio or if one sector exceeds 25%, it’s time to rebalance. You can trim oversized positions and redirect those funds to underweighted areas. Alternatively, you might temporarily stop automatic reinvestment for overweight stocks and use those dividends to invest in underrepresented sectors. This way, you maintain diversification without triggering unnecessary trades.

Here’s a quick reference table to guide your portfolio management:

| Metric | Target Range | Why It Matters |

|---|---|---|

| Payout Ratio | 30% – 60% | Ensures sustainability and room for growth |

| Review Frequency | Every 6–12 months | Prevents overreacting to short-term volatility |

| Individual Stock Weight | 2% – 5% | Limits the impact of any single stock |

| Sector Allocation | < 25% per sector | Protects against industry-wide downturns |

Tools and Resources for Dividend Investors

Stock Screening Platforms

When it comes to finding reliable dividend stocks, DividendData.com stands out with its AI-powered screener. It uses over 30 years of historical data to evaluate dividend safety, focusing on critical metrics like Free Cash Flow and Net Income payout ratios. This method ensures you’re targeting stocks with sustainable dividend growth. As investor Garrett Ray describes it:

"The best ‘all-in-one’ resource for tracking my existing DRIP portfolio, projecting what my annual dividend income stream will look like… and visualizations of how that income stream has grown over time".

Another excellent resource is Dividend.com, which employs a proprietary rating system to score stocks on a scale of 1 to 5, based on their reliability and yield appeal. For instance, as of January 16, 2026, their screener highlighted the stark contrast between growth and income stocks – NVIDIA (NVDA) offered a mere 0.02% yield, while Chevron (CVX) provided a robust 4.11%. The platform also organizes stocks into helpful categories like "Aristocrats" (25+ years of dividend increases), "Kings" (50+ years), and "Achievers" (10+ years), making it easier to identify dependable payers.

Charles Schwab is another solid option, offering stock and ETF screeners that include filters for payout ratios and current ratios. For example, you can focus on companies with a current ratio of 2 or higher, signaling strong short-term financial health. Schwab also tracks dividend growth history, a key factor for spotting companies with a consistent record of increasing payouts.

These platforms are invaluable for narrowing down your search and ensuring you’re investing in companies with reliable dividend performance.

Portfolio Tracking Tools

Once you’ve built your dividend portfolio, tracking its performance is essential to achieving your passive income goals. Tools like DividendData.com simplify this process by allowing you to link US brokerage accounts and monitor unlimited positions in one place. The platform offers detailed income forecasting, breaking down expected dividend payments annually, quarterly, monthly, and even daily – helpful for planning your cash flow.

These tools also calculate Yield on Cost (YOC), giving you a clear picture of your actual return as dividends grow over time. Additionally, they track compound annual growth rates (CAGR) for dividends over periods of 1, 3, 5, and 10 years. Visualizations of these metrics highlight the "snowball effect" of reinvested dividends, which can be a motivating factor during market fluctuations.

To maintain a balanced portfolio, these platforms also offer diversification analysis, ensuring no single sector accounts for more than 25% of your holdings. This helps protect your income stream from sector-specific risks. With these tools, you can regularly review and adjust your portfolio, keeping it aligned with your long-term passive income strategy.

Conclusion: Your Path to Passive Income

Building a dividend portfolio takes time, patience, and thoughtful decisions. As Investopedia aptly states, "A great income portfolio – or any portfolio for that matter – takes time to build". It’s perfectly normal to spend years fine-tuning the right mix of reliable, income-generating stocks.

To get started, focus on companies with a strong track record of paying dividends, aim for payout ratios below 60%, and diversify your holdings across 20 to 30 stocks in five to seven different industries. If your goal is to generate $1,000 in monthly passive income ($12,000 annually), you’ll generally need a portfolio of approximately $300,000 at a 4% dividend yield. Begin with what you can afford, and steadily grow your portfolio through regular contributions and reinvesting dividends.

Once your framework is in place, reinvestment becomes a powerful tool. Automating your investments through Dividend Reinvestment Plans (DRIPs) can take the guesswork out of the process, allowing compounding to quietly work in your favor. Instead of watching stock prices daily, schedule portfolio reviews every 6 to 12 months. During these check-ins, confirm that your companies are still increasing dividends, payout ratios remain stable, and no single sector dominates more than 25% of your portfolio.

Steer clear of chasing dividend yields above 10%, as these often indicate underlying financial issues. Instead, look for blue-chip companies offering yields in the 4% to 5% range and backed by strong balance sheets. Holding high-yield assets in tax-advantaged accounts can also help maximize your returns over time.

FAQs

How can I avoid falling for a ‘yield trap’ when picking dividend stocks?

To steer clear of a yield trap, don’t get lured in by an unusually high dividend yield alone. Take a closer look at the company’s payout ratio. If most – or all – of its earnings are being handed out as dividends, that could spell trouble. Make sure the dividend is backed by free cash flow and check whether the company’s earnings are stable or, better yet, on the rise. Watch out for high debt levels too, as they can chip away at profitability and even force dividend cuts. Sticking with companies that show solid financial health and steady performance can help you avoid these pitfalls.

What are the advantages of using Dividend Reinvestment Plans (DRIPs)?

Dividend Reinvestment Plans, or DRIPs, let you automatically reinvest your dividends into more shares of the same stock, including fractional shares. The best part? This is usually commission-free or even offered at a discount, making it a cost-effective way to grow your investments over time.

Reinvesting dividends taps into the power of compounding – where your earnings start generating their own earnings. It’s a simple, hands-off strategy that can boost your long-term returns, whether your goal is to build passive income or steadily grow your portfolio.

How can I keep my dividend portfolio diversified and balanced?

To keep your dividend portfolio balanced and diversified, start by defining clear allocation goals. Decide how much of your investments will go into dividend-paying stocks, bonds, and cash. Spread your investments across various sectors like technology, utilities, and consumer staples to avoid putting all your eggs in one basket and reduce the risk of being overly dependent on a single sector.

Dividend-focused ETFs can be a great way to achieve diversification quickly. These funds group multiple high-quality dividend-paying stocks into a single investment, simplifying the process. If you prefer picking individual stocks, make sure to select companies from different industries and market sizes. To manage risk, try to keep any single stock at about 5-10% of your portfolio.

Make it a habit to review your portfolio at least every quarter. If you notice a stock or sector taking up too much space, rebalance by selling some of the overweight positions and redirecting those funds to areas that are underrepresented. Lastly, consider setting up automatic dividend reinvestment. This approach allows you to compound your returns while staying aligned with your allocation strategy.