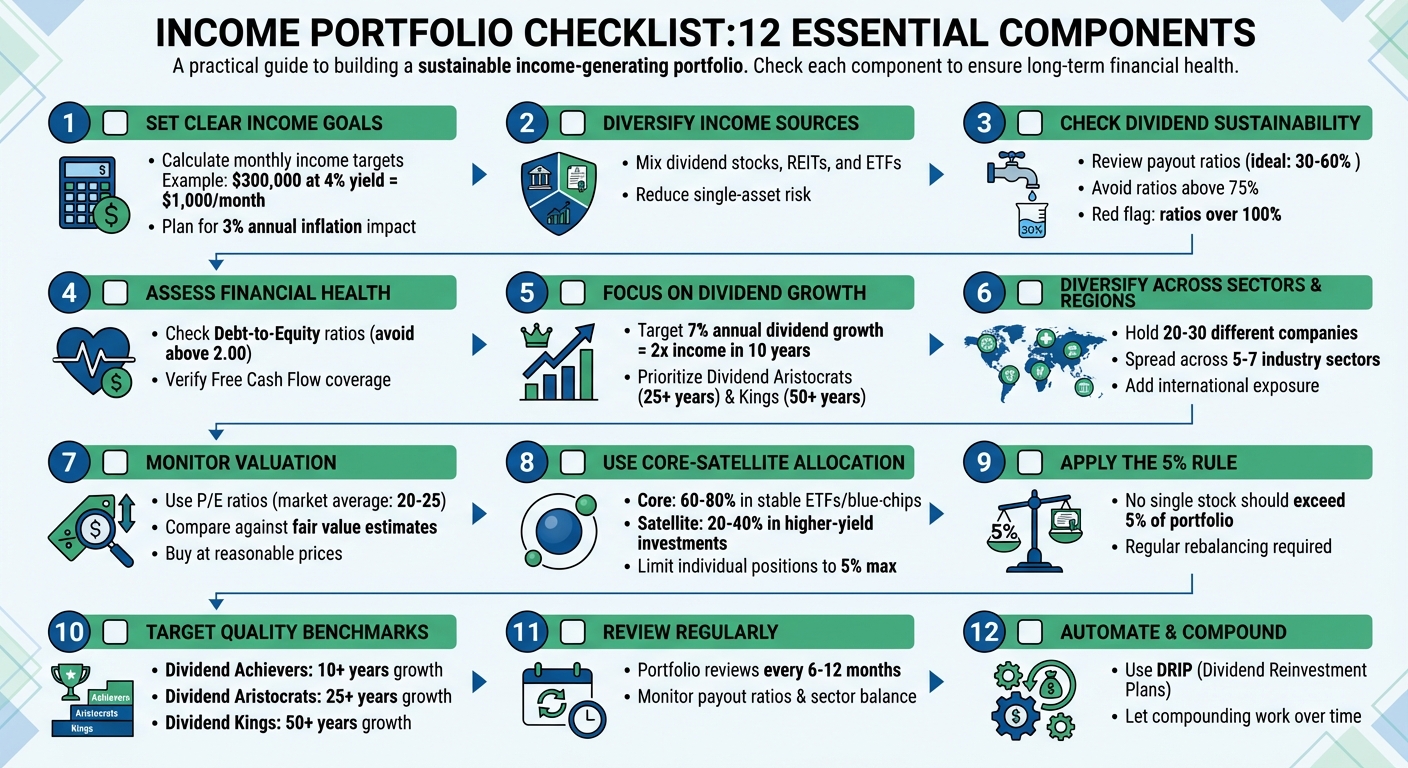

Income Portfolio Checklist: 12 Essential Components

Building an income portfolio that generates reliable cash flow isn’t just about picking high-yield investments. It’s about creating a balanced plan that delivers steady income now while protecting your financial future. Here’s a quick summary of the key steps to take:

- Set Clear Income Goals: Determine how much monthly income you need and calculate the portfolio size based on expected yields (e.g., $300,000 at 4% yield for $1,000/month).

- Diversify Income Sources: Spread investments across dividend stocks, REITs, and ETFs to reduce risk and maintain stability.

- Check Dividend Sustainability: Evaluate payout ratios and cash flow to ensure dividends are reliable and not at risk of cuts.

- Assess Financial Health: Review companies’ debt-to-equity ratios and free cash flow to confirm their ability to maintain payouts.

- Focus on Dividend Growth: Prioritize companies with long histories of increasing dividends, like Dividend Aristocrats and Kings.

- Diversify Across Sectors and Regions: Avoid overconcentration by investing in multiple sectors and international markets.

- Monitor Valuation: Buy stocks at reasonable prices to maximize yield and limit risk.

- Use Core-Satellite Allocation: Build a stable core (60–80%) with ETFs or blue-chip stocks and add higher-yield satellite investments (20–40%).

12 Essential Components of an Income Portfolio Checklist

Build $1,000/Month in Dividends: A 5-Step Framework

1. Set Clear Income Goals

Before diving into investments, you need to figure out exactly how much income you’ll need. This number drives everything – your asset choices, risk tolerance, and overall strategy. Without a clear target, building a portfolio becomes a shot in the dark.

Calculate Monthly Income Targets

Start by tallying up your monthly expenses and identifying any income gaps. For example, if you need $1,000 per month in passive income (or $12,000 annually), you’ll need about $300,000 invested at a 4% dividend yield or $200,000 at a 6% yield. To find the portfolio size you need, divide your annual income goal by the expected dividend yield.

Your timeline also plays a key role. If you’re decades away from needing income, growth stocks may be a better option to build capital. But if you’re nearing retirement or need income within the next five years, it’s smarter to focus on more conservative, income-generating assets.

"Knowledge is power, but you don’t have to become a financial prodigy to set yourself up for long-term success".

Taxes also matter. Bond interest is taxed at ordinary income rates, which could be 30% or more, while qualified dividends usually enjoy lower rates – around 15%.

Plan for Inflation

Don’t forget to factor in inflation when setting your targets. A fixed income stream loses buying power over time. For instance, at a 3% inflation rate, $50,000 in annual income will shrink to the equivalent of just $35,000 in 12 years. Ignoring inflation can seriously erode your long-term financial stability.

To combat this, consider investing in Dividend Aristocrats – companies that have increased their dividends for 25 consecutive years – or Dividend Achievers, which have a 10+ year track record of raising payouts. These types of companies naturally hedge against inflation by growing their dividends. For example, a company increasing its dividend by 7% annually will double your income stream in just 10 years.

2. Diversify Your Income Sources

Once you’ve set clear income goals, the next step is to protect your cash flow by diversifying your investments. Relying too heavily on a single asset type can leave you vulnerable to market swings. By spreading your investments across different assets, sectors, and regions, you can create a more stable and reliable income stream. For instance, if dividend stocks underperform, REITs might hold steady, or if U.S. markets take a hit, international investments could help balance the impact.

Take the 2008–2009 financial crisis as an example. A diversified portfolio with 70% stocks, 25% bonds, and 5% short-term investments performed better than less balanced approaches. The goal here isn’t to chase the highest returns – it’s about protecting your portfolio and maintaining consistent income, especially during turbulent times.

Mix Dividend Stocks and REITs

Dividend stocks are a cornerstone for steady income and potential capital growth. Companies with a history of increasing payouts provide a buffer against inflation, making them a reliable choice for income-focused investors.

Adding REITs (Real Estate Investment Trusts) to the mix can further strengthen your portfolio. By law, REITs must pay out at least 90% of their taxable income as dividends, which often results in higher yields compared to traditional stocks. For instance, the median dividend yield for Dividend Aristocrats in early 2025 was about 2.25%, whereas the S&P 500 average yield was closer to 1.3%. Beyond their yields, REITs offer a unique advantage: they often don’t move in sync with stocks or bonds. Plus, since rents typically rise with inflation, REITs can act as a natural hedge against increasing costs. Combining dividend stocks and REITs can boost both your income and the overall stability of your portfolio.

Add ETFs for Broad Exposure

If picking individual stocks or REITs feels overwhelming, ETFs (Exchange-Traded Funds) provide a simple and effective alternative. With ETFs, you can invest in a basket of securities, instantly spreading your risk across multiple companies and sectors. This diversification means that if one company cuts its dividend, the impact on your overall income remains small.

"If you can’t find the needle, buy the haystack." – Vanguard

ETFs also come with lower fees and professional management, making them a cost-effective option that requires less hands-on monitoring.

Geographic diversification is another essential piece of the puzzle. While the U.S. accounts for 63% of global market value, it represents just 25% of the global economy. Adding international ETFs to your portfolio reduces the risk of overconcentration in U.S. markets. This is particularly important given the growing dominance of U.S. tech and AI stocks, as seen in the Morningstar US Market Index, where the top 10 companies’ weight increased from 23% to 36% over the past five years. International exposure helps balance these trends and spreads your risk across a broader economic landscape.

3. Check Dividend Sustainability

A high dividend yield might seem appealing at first glance, but it’s meaningless if the company can’t sustain those payouts over time. Before you add any stock to your income portfolio, it’s crucial to confirm that the dividend is stable – not just now, but through the inevitable ups and downs of the market.

The best way to do this is by diving into the company’s financial health. If a company is overextended or paying out more than it earns, it’s a warning sign for income stability. Let’s break down the key factors to evaluate dividend sustainability.

Review Payout Ratios

The payout ratio is a simple but powerful metric – it shows what percentage of a company’s earnings are used to pay dividends. You can calculate it by dividing the annual dividend per share by the earnings per share (EPS). Generally, a payout ratio in the range of 30% to 60% is considered balanced. This range allows companies to retain enough cash for growth while maintaining dividend payments.

However, when payout ratios exceed 75%, the company has little room to maneuver if earnings drop. If the ratio goes over 100%, it’s a major red flag – this means the company is paying out more than it earns, which is unsustainable. For instance, while 3M kept its payout ratios between 44.8% and 72.7% over seven years, International Paper hit a concerning 167.3%, signaling trouble ahead.

"There is little point in seeking out dividend-paying stocks unless the dividend is secure and expected to grow." – Derek Hageman, AAII

Another crucial metric is the Free Cash Flow (FCF) payout ratio, which focuses on actual cash flow rather than accounting profits. Dividends are paid in cash, not just paper earnings, so this ratio offers a clearer picture of whether a company has the liquidity to sustain payouts. Texas Instruments (TXN), for example, aims for an FCF payout ratio between 40% and 60%, giving investors confidence in its financial transparency.

It’s also important to compare a company’s payout ratio to its industry norms. For example, REITs (Real Estate Investment Trusts) are required by law to distribute at least 90% of their taxable income, so high payout ratios are expected. But for typical corporations, those same ratios could signal trouble.

Regularly reviewing these ratios can help you reduce risks and build a more reliable income portfolio.

Avoid Companies with Dividend Cuts

Beyond the numbers, a company’s dividend history speaks volumes about its ability to maintain payouts. If a company has cut or suspended its dividend in the past, it’s a red flag that management either can’t sustain payments during tough times or doesn’t prioritize shareholders.

"Dividends tend to be ‘sticky.’ Once a dividend payment is established, companies are under pressure to maintain and increase the payment." – Derek Hageman, AAII

When dividends are reduced, stock prices often tumble, eroding investor confidence. That’s why the most reliable income stocks are those with long histories of uninterrupted – or better yet, increasing – dividend payments. Dividend Aristocrats, which have raised dividends for 25+ consecutive years, and Dividend Achievers, with 10+ years of increases, have proven their resilience through recessions, market crashes, and global crises.

Take Altria Group (MO), for example. As of January 2026, it has raised its dividend for 54 straight years, weathering events like the Dot-Com Bubble, the 2008 Financial Crisis, and the 2020 Pandemic. Another example is Bank of America (BAC), which rebounded from the 2008 crisis by increasing its quarterly dividend from $0.01 per share in 2011 to $0.21 per share by 2021 – a 20x growth in a decade.

The broader data supports this: during the 2020 global pandemic, only 7% of U.S. companies in the Janus Henderson Global Dividend Index cut or canceled their dividends, while more than 90% either maintained or increased their payouts. Companies with strong dividend histories tend to stay committed to their shareholders.

When building your income portfolio, make it a rule to avoid companies that have recently reduced or suspended dividends. Past actions often provide the clearest insight into a company’s priorities and financial durability.

4. Evaluate Balance Sheet Strength

A company’s dividend history doesn’t mean much if its balance sheet can’t hold up under pressure. A solid balance sheet is the backbone of reliable dividend payments, especially during recessions, market swings, or economic downturns.

While a strong dividend track record highlights past performance, the balance sheet tells you whether those payouts are likely to continue. To gauge this, you’ll need to dig into the company’s financial health and determine if it has the resources to sustain its dividend payments.

Check Debt-to-Equity Ratios

The Debt-to-Equity (D/E) ratio – calculated by dividing total liabilities by shareholder equity – offers insights into how much debt a company is carrying. This matters because debt creates fixed obligations that must be paid before dividends can be distributed.

"High debt is the number one threat to a dividend during a recession." – Investing.com

In tough economic times, companies with heavy debt often face the tough choice of prioritizing debt repayment over dividends. As a general rule, steer clear of companies with D/E ratios above 2.00. That said, acceptable levels of leverage can differ by industry. For instance, in August 2021, Allstate Corp (ALL) operated with a liabilities-to-assets ratio of 78.7%, which is typical for the insurance sector, while maintaining a conservative dividend payout ratio of 18.9%. On the other hand, Snap-on Incorporated (SNA) showed strong financial health with a liabilities-to-assets ratio of 41.1% and a payout ratio of 32.7%.

Verify Free Cash Flow Coverage

Dividends aren’t paid with accounting profits – they’re paid with actual cash. That’s why Free Cash Flow (FCF), which represents the cash left after covering operating costs and capital expenditures, is a critical metric for evaluating dividend safety.

"Because dividends are paid in cash, not accounting profits, this [cash payout] ratio is often a better indicator of dividend safety than earnings alone." – Jason Hall, The Motley Fool

To check FCF coverage, calculate the Cash Payout Ratio by dividing common stock dividends by the cash flow from operations minus capital expenditures (and subtracting any preferred dividends if applicable). A lower ratio means the company has more breathing room to maintain its dividend. Additionally, a Dividend Coverage Ratio (DCR) above 2.0x is generally a good sign, while a ratio consistently below 1.5x could signal trouble.

For example, in 2015, Procter & Gamble demonstrated sound financial management by keeping net interest expenses at $626 million – less than 10% of its $7 billion net income – ensuring it could comfortably sustain its dividend. When evaluating dividend-paying stocks, it’s essential to confirm that payouts are well-supported by Free Cash Flow to Equity (FCFE), rather than relying solely on accounting profits.

sbb-itb-484be5d

5. Look for Consistent Dividend Growth

Once you’ve confirmed a company’s dividend sustainability and financial stability, the next step is to focus on consistent dividend growth. A strong balance sheet is important today, but steady dividend increases signal resilience for the future. Companies that consistently raise their dividends – even during economic downturns like recessions, market crashes, or global crises – show a clear commitment to rewarding shareholders. This consistency often proves more rewarding than chasing a high current yield.

"A 25-year streak means the company navigated the Dot-Com Bubble, the 2008 Financial Crisis, and the 2020 Pandemic without cutting its dividend. This history is the single best predictor of future resilience." – Investing.com

Growing dividends also act as a hedge against inflation. For example, a company increasing its dividend by 7% annually will double your income stream every 10 years. Compare that to a stagnant 6% yield, which loses purchasing power over time as inflation erodes its value. A modest starting yield of 3%, paired with strong growth of 5-10% per year, can eventually outpace a higher but flat 6% yield. The growth rate is the real driver of compounded income, making it a critical factor when evaluating dividend-paying stocks.

Target Dividend Aristocrats and Kings

Dividend-paying companies are often grouped into categories based on their reliability and track record. These categories, such as Dividend Achievers, Aristocrats, and Kings, help investors identify businesses with a history of consistent payouts.

- Dividend Achievers: Companies that have increased their annual dividend for at least 10 consecutive years.

- Dividend Aristocrats: A select group of S&P 500 companies with 25 or more consecutive years of dividend growth.

- Dividend Kings: The top tier, consisting of companies with 50 or more years of consecutive dividend increases.

As of January 2026, there are 67 Dividend Aristocrats, which have historically outperformed the S&P 500 on a risk-adjusted basis over the long term. Examples include:

- Dover Corporation (DOV): 71 years of consecutive dividend growth, offering a 1.01% yield with a stock price of $206.61.

- Target Corporation (TGT): 55 years of dividend growth, with a 4.10% yield and a stock price of $111.28.

- PepsiCo (PEP): 54 years of dividend growth, delivering a 3.89% yield and an annual dividend of $5.69 per share as of January 2026.

These companies have demonstrated their ability to navigate economic challenges while maintaining their dividend commitments, making them reliable choices for income-focused investors.

Confirm 20-Year Growth History

While a 10-year dividend growth streak is impressive, a 20-to-25-year history is the ultimate benchmark for resilience. This longer timeframe shows that a company has successfully weathered multiple economic cycles, including at least two major recessions. For those building a retirement income portfolio or seeking steady cash flow, companies with this kind of track record are essential.

One key metric to evaluate is the Dividend CAGR (Compound Annual Growth Rate). A high CAGR over 10 years not only drives income growth but also helps protect against inflation. For example, Walmart Inc. (WMT) has maintained a 53-year streak of dividend increases as of January 2026. This kind of long-term growth reflects strong financial health and a commitment to rewarding shareholders.

When assessing potential investments, check that payout ratios generally stay between 30% and 60% for most companies. It’s also crucial to ensure dividends are covered by Free Cash Flow rather than just accounting earnings. For instance, as of January 2026, PepsiCo offers a forward yield of 4.07%, with analysts projecting its payout ratio to remain in the low 70s and annual dividend growth to continue at a steady mid-single-digit rate over the next decade. This balance of reasonable payout ratios and consistent growth is exactly what income-focused investors should prioritize.

"Dividend aristocrats provide a steady and rising passive income that can help take the sting out of inflation, be less reliant on stock prices going up, and weather market downturns with fewer portfolio swings." – Investopedia

6. Follow Diversification Rules

Even the most reliable dividend-paying stocks can stumble, especially if your portfolio is concentrated in just a few holdings. A single company’s dividend cut or an entire sector facing challenges could disrupt your cash flow. The solution? Spread your investments across multiple stocks, sectors, and regions.

For a well-rounded dividend portfolio, aim to hold 20 to 30 different companies. At the very least, include 12 individual stocks to achieve a baseline level of diversification. Beyond that, allocate your investments across 5 to 7 industry sectors – such as utilities, healthcare, real estate investment trusts (REITs), and consumer staples. This approach shields your portfolio from downturns specific to any one sector. These diversification guidelines build on earlier strategies by emphasizing limits on individual holdings and geographic exposure.

Limit Individual Holdings

A common rule of thumb for managing risk is the 5% rule: no single stock should make up more than 5% of your portfolio. For example, if a single stock’s value grows and begins to account for 10% of your portfolio, it’s time to trim it back to the 5% target. This ensures your portfolio remains balanced and less vulnerable to market surprises.

Regular rebalancing is key. Without it, strong performers could dominate your portfolio, exposing you to unnecessary risk.

Diversify Geographically

Geographic diversification is another important layer of protection. It reduces dependence on any one country’s economy or regulatory environment. Adding international dividend stocks or exchange-traded funds (ETFs) can help you tap into different economic trends and currencies, potentially stabilizing returns when U.S. markets hit a rough patch.

"One company, one sector, one currency, or one region could find itself worse off in a new world order, so now is a great time to put some eggs in other baskets." – Bryan Armour, Director of ETF and Passive Strategies Research, Morningstar

International mutual funds or ETFs offer an easy way to gain exposure to a wide range of foreign companies, minimizing risks tied to any single issue. A simple strategy to achieve this is the three-fund portfolio: one domestic stock fund, one international stock fund, and one fixed-income fund. This setup provides broad coverage across geographic regions and asset classes.

However, keep in mind that international investments also come with currency risk. Fluctuations in exchange rates can impact the value of your income when converted back to U.S. dollars. Balancing these risks with the benefits of global diversification is key to building a resilient portfolio.

7. Monitor Valuation for Entry Points

Even the best dividend stocks can lead to disappointing results if you overpay. The price you pay is just as crucial as picking the right company. When a stock trades below its fair value, you not only secure a higher yield but also increase your chances of capital growth. To assess whether a stock is priced attractively, use standard valuation ratios.

Use Price-to-Earnings Ratios

Getting the right entry price can boost your income while minimizing risk. The Price-to-Earnings (P/E) ratio measures how much you’re paying for each dollar of a company’s earnings. It’s calculated by dividing the stock price by its earnings per share (EPS). Typically, the average P/E ratio for the market falls between 20 and 25.

A lower P/E compared to industry peers or historical averages often signals an undervalued stock. However, always compare P/E ratios within the same sector – what’s considered typical for a utility company can differ significantly from a tech firm. For instance, in August 2025, Walmart was trading at $99.31 with a trailing GAAP EPS of $2.34, resulting in a P/E of 42.44. Using adjusted EPS of $2.51 (which excludes one-time events), the adjusted P/E dropped to 39.57, offering a clearer picture of its ongoing business performance.

The PEG ratio (Price/Earnings-to-Growth) refines this further by incorporating expected earnings growth. A PEG ratio below 1.0 often indicates a stock is undervalued relative to its growth potential.

Compare Against Fair Value Estimates

Fair value estimates provide a benchmark that focuses on a company’s fundamentals rather than market hype. Analysts calculate this by projecting future cash flows and discounting them back to their present value. Tools like Bullish Flow’s fair value analysis can help you spot stocks trading below their intrinsic worth.

The dividend yield approach is particularly effective for stable, mature companies. To find a "normal" price range, divide the expected annual dividend by the stock’s historical high and low dividend yields. For growth-oriented dividend stocks, multiply historical P/E ranges by projected earnings for the next year to establish a value range.

"A stock being overvalued doesn’t mean it’s not a good stock to own – it just means it’s not the right time to buy it." – Morningstar

Finally, ensure that dividends are backed by Free Cash Flow rather than just accounting profits. This helps confirm that the dividends are sustainable over time.

8. Use Core-Satellite Allocation

Creating a balanced income portfolio involves blending stable, reliable assets with higher-yield investments. This is where the core-satellite approach comes in. It divides your portfolio into two parts: a solid foundation (the core) and smaller, targeted investments (the satellites). Typically, the core makes up 60–80% of your portfolio, focusing on low-volatility, dependable dividend payers like broad-market ETFs or blue-chip stocks. The remaining 20–40% is allocated to satellites – higher-yield assets such as REITs, Business Development Companies (BDCs), or sector-specific plays that can enhance your overall income potential. This strategy not only diversifies your portfolio but also ensures a clear separation between steady income sources and higher-yield opportunities.

"The ‘Core’ is the sun in your financial solar system… Its primary job is to preserve your capital and generate a steady, predictable stream of dividend income." – Curtis Reker, Founder, Dividend Yield Seeker

Your allocation should align with your risk tolerance and financial goals. For example, conservative investors nearing retirement might allocate 80–90% to core assets, while those building wealth may aim for 70–80% core. If you have a longer investment horizon and a higher risk tolerance, you might consider a 60–70% core allocation. The key is to assess your comfort level honestly – if market fluctuations make you uneasy, a larger core allocation can provide peace of mind.

Allocate 60–70% to Stable ETFs

Your core holdings should form the backbone of your income strategy, offering stability and consistent returns. Broad-market dividend ETFs, such as the Schwab U.S. Dividend Equity ETF (SCHD), are excellent options. In 2025, SCHD provided a yield of approximately 3.8% with a low 0.06% expense ratio, offering diversification across quality dividend-paying companies along with predictable quarterly cash flow. Dividend Aristocrats, known for their long track record of increasing payouts, are also strong candidates for core holdings. While their yields might be lower, their reliability and reduced volatility help safeguard your capital during market downturns.

Add High-Yield Opportunities as Satellites

Satellites are where you can take calculated risks to boost your income. These might include REITs, BDCs, or covered-call ETFs like the JPMorgan Equity Premium Income ETF (JEPI), which yielded about 8.4% in June 2025. To manage risk, limit individual satellite positions to 2–5% of your total portfolio. Be cautious with assets yielding over 10%, as they often come with weak fundamentals and a higher likelihood of dividend cuts. For better tax efficiency, consider holding these high-yield assets in tax-advantaged accounts like IRAs, as their distributions are taxed at ordinary income rates.

Conclusion

Creating a dependable income portfolio isn’t about chasing the highest yields – it’s about building a well-rounded system that works together. The 12 components in this checklist act as interconnected parts: your income goals and inflation planning set the direction, diversification and core-satellite allocation provide the structure, and sustainability checks serve as the safety net to avoid risky dividend traps. At the same time, dividend growth drives compounding, helping your income keep up with inflation over the years.

Each piece of the portfolio plays a specific role. Diversification reduces risk, while monitoring valuations ensures smart entry points. Think of diversification as your portfolio’s shock absorber – by capping any single position at 5% of your total portfolio, you protect your income stream from being derailed if one investment underperforms. Valuation monitoring ensures you’re buying at prices that maximize your yield-on-cost while minimizing potential losses. The core-satellite strategy strikes a balance, allocating 60–70% of your portfolio to broad ETFs for stability while using individual stocks to achieve higher yields without taking on excessive risk.

"A well-built dividend plan blends safety and sizzle – steady growers and reliable payers." – Dividend.Direct

Automation can make this process much easier. Dividend Reinvestment Plans (DRIP) allow you to reinvest earnings automatically, turning small amounts into substantial growth over time. Regular portfolio reviews every 6–12 months help ensure payout ratios remain sustainable and sector allocations stay balanced.

Take advantage of tools like Bullish Flow’s research features. Use screeners to find Dividend Achievers or Aristocrats, set filters for payout ratios below 60%, and benchmark debt-to-equity ratios. These tools simplify analysis and help guide your decisions. Scenario projections with dividend calculators can show when you’ll reach specific income goals, while earnings analysis and real-time tracking keep your portfolio on course.

Start small – define your income goals and build a core allocation with stable ETFs. Gradually add satellite investments, check sustainability metrics, and let the power of compounding work in your favor. By following these steps, you’ll solidify the framework outlined in this checklist. Achieving financial stability through dividend income doesn’t have to be overwhelming; it just takes consistency and the right approach.

FAQs

How do I choose the best asset allocation for my income portfolio?

Choosing the right mix for an income portfolio starts with understanding three key factors: your income needs, time horizon, and risk tolerance. Think about how much cash flow you’ll need, how long you’ll rely on it, and how comfortable you are with market ups and downs. These considerations shape how you divide your investments among dividend-paying stocks, REITs, bonds, and cash equivalents.

A typical allocation might look like this: 30-50% in dividend stocks and REITs to provide a mix of growth and income, 20-40% in bonds or bond ETFs for added stability, and 5-10% in cash or short-term government securities for quick access to funds. If you’re more risk-averse, you might lean toward a higher percentage of bonds. On the other hand, if you can handle more market volatility, you could increase your allocation to dividend stocks.

After setting your allocation, make it a habit to review your portfolio every year – or sooner if your financial needs or market conditions shift. Regular rebalancing helps keep your investments aligned with your goals and ensures your income stream remains steady.

What risks should I consider when investing heavily in high-yield assets?

Investing heavily in high-yield assets comes with its fair share of risks. One of the most pressing concerns is default risk – the possibility that issuers might fail to meet their financial obligations. Then there’s price volatility, which tends to be more pronounced in high-yield investments, potentially leading to unpredictable swings in your portfolio’s value. Overloading on high-yield options can also introduce concentration risk, making your investments less diversified and more susceptible to market declines.

Another pitfall to watch out for is the high-yield trap. This happens when an asset’s high yield isn’t sustainable, often hinting at deeper financial troubles within the issuer. If the yield suddenly drops or the issuer defaults, the impact on your portfolio’s returns and overall stability can be substantial. To navigate these challenges, aim for a well-balanced, diversified portfolio and take the time to thoroughly assess the quality and long-term viability of high-yield investments.

How does investing in different regions improve the stability of my income portfolio?

Geographic diversification is a smart way to bring stability to your income portfolio. By spreading your investments across different countries and regions, you reduce the risk of being overly dependent on a single economy. This means you’re less vulnerable to challenges like political upheavals, regulatory changes, or economic slowdowns in one area. For instance, if one market struggles, income from investments in other regions can help balance things out, providing a steadier cash flow.

Incorporating dividend-paying stocks, REITs, or ETFs from both U.S. and international markets adds another layer of resilience. It not only helps smooth out regional volatility but also opens the door to opportunities in regions that may offer better yields or more predictable income patterns. To keep your portfolio working effectively, it’s important to regularly review and adjust it, ensuring it aligns with your financial goals while continuing to deliver a reliable income.